March saw the value of the portfolio decline, largely in line with the movements in equity markets and adverse exchange rate movements. Positive cash from on the properties (fully leased) only partly offset the losses elsewhere. Savings for the month were negative - and I cannot recall the last time that happened.

Here are the details:

1. my Hong Kong equity portfolio fell. I purchased shares in CKI Holding, BCIA, Tibet 5100, Cosco Pacific and CNOOC;

2. my AU/NZ equities were flat;

3.my ETFs fell in line with the local markets, with all being negative;

4. my commodities fell, led by silver;

5. all of my properties were occupied with all tenants paying on time. One property had a two week vacancy between tenancies and substantial costs were incurred in redecorating etc;

6. currency movements were negative, as the NZD and AUD fell against the HKD/USD;

7. my position in bonds remains small. No bonds were purchased this month. I would like to add some more bonds to the portfolio but am finding direct purchases of bonds through the banks I have accounts with to be something of an exercise in frustration in Hong Kong;

8. I had no open derivative positions;

9. savings were negative due to a combination of low income (March is usually the lowest month of the year) and high expenses (paying for our annual holiday in April, the personal expenses for a recent business trip to London, my life insurance premium for the year being paid and the annual premium for the family's medical insurance - of these only the holiday costs had been substantially provided for through my accruals).

My cash position declined due to new investments. I currently hold 49.3 months of expenses in HKD cash or equivalents. This is more than enough - in fact it is too high given current inflation levels and the near zero nominal yields on bank deposits.

For the month, my net worth fell by 1.47%. The year to date increase is 13.95%. The year is off to a good start and I remain on track to retire at the end of 2012.

Saturday, March 31, 2012

Friday, March 30, 2012

Tibet Water 5100 - partial sale

This morning I sold the shares in Tibet Water 5100 (HK:1115) which I had purchased at HK$1.82 on Wednesday for HK$1.89/1.90. The profit was 3.2% (net of costs) for a two day holding period. I still hold the remaining shares purchased at higher prices.

As an aside, I attempted to pick up some shares in SHK (HK:16) at HK$92.00 this morning on expectation of a big drop following the arrest of the company's two co-chairmen (among others) in a corruption scandal. Unfortunately, the shares only got as low as HK$94.00 so I missed out.

As an aside, I attempted to pick up some shares in SHK (HK:16) at HK$92.00 this morning on expectation of a big drop following the arrest of the company's two co-chairmen (among others) in a corruption scandal. Unfortunately, the shares only got as low as HK$94.00 so I missed out.

Thursday, March 29, 2012

Does Hong Kong really have a property bubble?

There is no shortage of talk about Hong Kong's property bubble. In fact people have been calling the local property market a bubble for a few years now. Commentary usually proceeds on the basis that there is a bubble and then moves on to talk about the risks and implications (either with or without predictions on when the bubble will burst).

My non-expert attempt to satisfy myself that there is in fact a bubble is set out below. The conclusion I reached is that while Hong Kong real estate is expensive my many (but not all) measures, I was struggling to find evidence that there was in fact a bubble in the Hong Kong housing market.

Characteristics of a bubble

Looking at the definition of "bubble" it is fairly obvious that at least some of the key characteristics of a bubble are absent. In particular transaction volumes are subdued (and have been since the government's cooling measures) rather than "high". Also, while expensive (see below) prices have at least a reasonable connection with intrinsic values - with short term speculators (flippers/confirmors) being largely excluded from the market, most buyers are either end users or longer terms investors. That buyer profile is not consistent with the crowd of frothy speculators

It's also worth mentioning that the high levels of gearing commonly associated with real estate bubbles is notably absent. HKMA and bank imposed deposit requirements are high and many buyers are paying cash. Higher interest rates would be unlikely to result in a large number of distressed mortgagors.

Property price index

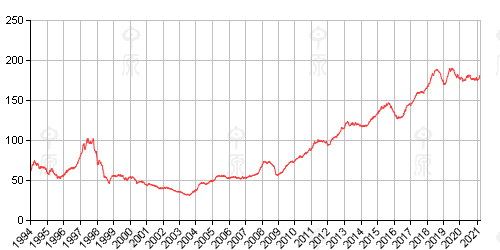

The leading index for the residential secondary market is the Centa-City Leading Index (CCL) published by Centadata which is available here. The chart below shows the CCL from 1994 through to 23 March, 2012.

It's worth noting that the CCL is based on actual sales prices in the secondary market. In other words it is a nominal index rather than a real (inflation adjusted index). Using Hong Kong CPI as a measure of inflation:

The CPI data is from Trading Economics which has some neat interactive features.

Very roughly, if the index was rebased to 1994 dollars, it would lower the 2012 value of the CCL by about 25.8% or from 99.17 to 78.83 and 1997's base CCL of 100 by 22.7% to 81.5%. In other words, from 1994 to 2102 in real terms the CCL rose from 63 to 99.17 (57.4%) in nominal terms and from 63 to 78.83 (25.1%) in inflation adjusted terms. Quite frankly, that's not much of a gain over a period of 18 years, especially when the expansion of Hong Kong's economy is taken into account. The compound annual increase in the value of the CCL (in either nominal or real terms) is small.

While it is just about always possible to quibble with the methodology used to construct an index, for present purposes, the only thing I will mention is that the CCL does not adjust for the size effect (the fact that larger properties typically sell for more per square foot than smaller ones). While I could not find any data tracking the average size of apartments in Hong Kong, anecdotally I understand that the average size has increased over time, although not by much. An adjustment to account for the size effect would reduce the rate of increase in the CCL.

Put differently, I would need to cherry pick the low point in the CCL in 2003 to show a reasonably high rate of annual increase in the CCL (and given that 2003 coincided with the end of the Asian Financial Crisis and SARS, it would indeed be an exercise in cherry picking the data).

Affordability

One way to measure whether real estate is expensive is affordability. Leaving aside reports like the one included in this article which are based on seriously flawed comparisons (at the very least there would need to be adjustments for differential tax rates and differential living costs - and in both respects Hong Kong does very well with most income earners paying no tax and not being burdened by the high cost of owning and running one or more private cars), it would appear that housing affordability today is much better than it was in 1997 (a combination of much lower interest rates and higher incomes) but worse than it was at the low point in 2003.

Given that (IMHO) high deposit requirements distort affordability comparisons even within Hong Kong, there isn't much point in debating the exact measures of affordability beyond the generalisations above. That said, it is not possible to claim that there is a bubble based on measures of affordability.

Other indicators

There is no denying that Hong Kong real estate is expensive in both absolute and relative terms. Hong Kong residential prices usually rank in the upper echelons of the global price bracket alongside cities like London and New York. Given Hong Kong's small size and status as a substantial financial centre, this is hardly surprising. Being expensive on a global comparative basis but no more so than several other cities does not a bubble make.

Yield is one yard stick used by investors to evaluate property as an investment. At the moment, gross yields on unfurnished mid-market units in good areas like Mid-Levels are in 3-5% range. Net yields are obviously lower and there is considerable variation between properties (as you would expect). Yields this low in an environment where inflation is 4.7%, bank deposit rates are negligible and mortgage rates are around 2.25% are both understandable and unexciting. In other words, it is possible to use at least some gearing and be cash flow positive on an investment property.

Conclusions

After going through the exercise, I failed to find anything that justified characterising Hong Kong's property market as a 'bubble' - none of the usual features of a bubble are present.

That said, real estate here is expensive (especially in the luxury sector) and I don't see enough value in the local market to justify adding to the portfolio. Given the political climate and the government stance on the property market as well as macro factors it is easy to see prices falling to some extent - how much is anybody's guess (and plenty of people are guessing). Given that affordability remains high and interest rates very low, it's also not beyond the realms of possibility that prices could go higher as well. Quite frankly, I have no idea.

Implications

As far as the implications of this exercise for my own investments are concerned, there aren't any. We will continue to hold our properties, collect the rent and reluctantly make the mortgage payments. We are unlikely to buy again at these levels - the value just isn't there. If prices drop far enough, we'd consider buying again. (And it goes without saying that just because prices drop by a meaningful amount in the future, that does not in any way validate claims that we have a bubble today.)

My non-expert attempt to satisfy myself that there is in fact a bubble is set out below. The conclusion I reached is that while Hong Kong real estate is expensive my many (but not all) measures, I was struggling to find evidence that there was in fact a bubble in the Hong Kong housing market.

Characteristics of a bubble

Looking at the definition of "bubble" it is fairly obvious that at least some of the key characteristics of a bubble are absent. In particular transaction volumes are subdued (and have been since the government's cooling measures) rather than "high". Also, while expensive (see below) prices have at least a reasonable connection with intrinsic values - with short term speculators (flippers/confirmors) being largely excluded from the market, most buyers are either end users or longer terms investors. That buyer profile is not consistent with the crowd of frothy speculators

It's also worth mentioning that the high levels of gearing commonly associated with real estate bubbles is notably absent. HKMA and bank imposed deposit requirements are high and many buyers are paying cash. Higher interest rates would be unlikely to result in a large number of distressed mortgagors.

Property price index

The leading index for the residential secondary market is the Centa-City Leading Index (CCL) published by Centadata which is available here. The chart below shows the CCL from 1994 through to 23 March, 2012.

It's worth noting that the CCL is based on actual sales prices in the secondary market. In other words it is a nominal index rather than a real (inflation adjusted index). Using Hong Kong CPI as a measure of inflation:

The CPI data is from Trading Economics which has some neat interactive features.

Very roughly, if the index was rebased to 1994 dollars, it would lower the 2012 value of the CCL by about 25.8% or from 99.17 to 78.83 and 1997's base CCL of 100 by 22.7% to 81.5%. In other words, from 1994 to 2102 in real terms the CCL rose from 63 to 99.17 (57.4%) in nominal terms and from 63 to 78.83 (25.1%) in inflation adjusted terms. Quite frankly, that's not much of a gain over a period of 18 years, especially when the expansion of Hong Kong's economy is taken into account. The compound annual increase in the value of the CCL (in either nominal or real terms) is small.

While it is just about always possible to quibble with the methodology used to construct an index, for present purposes, the only thing I will mention is that the CCL does not adjust for the size effect (the fact that larger properties typically sell for more per square foot than smaller ones). While I could not find any data tracking the average size of apartments in Hong Kong, anecdotally I understand that the average size has increased over time, although not by much. An adjustment to account for the size effect would reduce the rate of increase in the CCL.

Put differently, I would need to cherry pick the low point in the CCL in 2003 to show a reasonably high rate of annual increase in the CCL (and given that 2003 coincided with the end of the Asian Financial Crisis and SARS, it would indeed be an exercise in cherry picking the data).

Affordability

One way to measure whether real estate is expensive is affordability. Leaving aside reports like the one included in this article which are based on seriously flawed comparisons (at the very least there would need to be adjustments for differential tax rates and differential living costs - and in both respects Hong Kong does very well with most income earners paying no tax and not being burdened by the high cost of owning and running one or more private cars), it would appear that housing affordability today is much better than it was in 1997 (a combination of much lower interest rates and higher incomes) but worse than it was at the low point in 2003.

Given that (IMHO) high deposit requirements distort affordability comparisons even within Hong Kong, there isn't much point in debating the exact measures of affordability beyond the generalisations above. That said, it is not possible to claim that there is a bubble based on measures of affordability.

Other indicators

There is no denying that Hong Kong real estate is expensive in both absolute and relative terms. Hong Kong residential prices usually rank in the upper echelons of the global price bracket alongside cities like London and New York. Given Hong Kong's small size and status as a substantial financial centre, this is hardly surprising. Being expensive on a global comparative basis but no more so than several other cities does not a bubble make.

Yield is one yard stick used by investors to evaluate property as an investment. At the moment, gross yields on unfurnished mid-market units in good areas like Mid-Levels are in 3-5% range. Net yields are obviously lower and there is considerable variation between properties (as you would expect). Yields this low in an environment where inflation is 4.7%, bank deposit rates are negligible and mortgage rates are around 2.25% are both understandable and unexciting. In other words, it is possible to use at least some gearing and be cash flow positive on an investment property.

Conclusions

After going through the exercise, I failed to find anything that justified characterising Hong Kong's property market as a 'bubble' - none of the usual features of a bubble are present.

That said, real estate here is expensive (especially in the luxury sector) and I don't see enough value in the local market to justify adding to the portfolio. Given the political climate and the government stance on the property market as well as macro factors it is easy to see prices falling to some extent - how much is anybody's guess (and plenty of people are guessing). Given that affordability remains high and interest rates very low, it's also not beyond the realms of possibility that prices could go higher as well. Quite frankly, I have no idea.

Implications

As far as the implications of this exercise for my own investments are concerned, there aren't any. We will continue to hold our properties, collect the rent and reluctantly make the mortgage payments. We are unlikely to buy again at these levels - the value just isn't there. If prices drop far enough, we'd consider buying again. (And it goes without saying that just because prices drop by a meaningful amount in the future, that does not in any way validate claims that we have a bubble today.)

CNOOC purchased

In spite of it already being my largest holding, the combination of solid results and a falling share price prompted me to add a few more shares in CNOOC (HK:883) to the portfolio. Given the size of my position in this company, I will probably look to sell a few shares into the next rally.

I paid an average of HK$15.95 for the additional shares.

I paid an average of HK$15.95 for the additional shares.

COSCO Pacific purchased

With the share price dropping again this morning, I added a few more shares in Cosco Pacific (HK:1199) to the portfolio. I paid HK$11.60 for the additional shares.

Wednesday, March 28, 2012

COSCO Pacific purchased

This afternoon I purchased a few additional shares in COSCO Pacific (HK:1199) off the back of the release of their annual results.

I paid HK$12.00 for the additional shares.

I paid HK$12.00 for the additional shares.

Tibet 5100 purchased

This morning I added a few more shares in Tibet 5100 (HK:1115) to the portfolio. The company recently reported excellent results for the 2011 financial year, has an extremely strong balance sheet with no debt and lots of cash on hand, is diversifying its customer base, expanding its distribution network, has a high profit margin and does not have to spend huge amount of CAPEX to generate future growth. The only negatives were the rather miserly final dividend (HK$0.03) and the large receivable from a single customer.

Following the result the controlling shareholder placed just under 8% of of the issued shares into the market at HK$1.75 and the shares took a tumble (as expected). Since this wasn't dilutive (unlike wealth destroying placements of new shares) and the controlling shareholder still holds 43% of the company's shares, I took this as an opportunity to add to my position.

I paid HK$1.82 for the additional shares.

Following the result the controlling shareholder placed just under 8% of of the issued shares into the market at HK$1.75 and the shares took a tumble (as expected). Since this wasn't dilutive (unlike wealth destroying placements of new shares) and the controlling shareholder still holds 43% of the company's shares, I took this as an opportunity to add to my position.

I paid HK$1.82 for the additional shares.

Wednesday, March 21, 2012

Top ten individual equities

As an update, here is a list of the ten largest individual equities in the portfolio. Prices are from this morning (21st March) and the allocation is expressed as a percentage of the combined household balance sheet with most properties maked to most recent on-line mortgagee valuations.

The following also have a weighting of 0.6% but fall just outside the top ten list: Yanzhou Coal (HK:1171), Sino Oil & Gas (HK:702), China Metal Recycling (HK: 773), Fairwood (HK:52) and K Wah (HK:173).

| Rank | Company | Code | Allocation |

| 1 | CNOOC | 883 | 1.7% |

| 2 | Hutchison | 13 | 1.4% |

| 3 | Sinopec | 883 | 1.3% |

| 4 | China Gas | 384 | 1.3% |

| 5 | CCB | 939 | 1.1% |

| 6 | CKI | 1038 | 0.8% |

| 7 | Westpac | NA | 0.7% |

| 8 | Hua Han | 1188 | 0.7% |

| 9 | HKR International | 480 | 0.6% |

| 10 | GDI | 1102 | 0.6% |

The following also have a weighting of 0.6% but fall just outside the top ten list: Yanzhou Coal (HK:1171), Sino Oil & Gas (HK:702), China Metal Recycling (HK: 773), Fairwood (HK:52) and K Wah (HK:173).

Monday, March 19, 2012

BCIA purchased #2

This afternoon I added a few more BCIA (HK:694) to the portfolio. I paid HK$4.20 for the additional shares.

Thursday, March 15, 2012

BCIA purchased

I added a few shares in BCIA (HK:694) to the portfolio this afternoon. At first glance, BCIA is not the sort of stock I would be interested in - it has high levels of debt (much of which falls due in 2015, 2016 and 2017), a modest ROE, is selling at a trailing PE of 25x and had a patchy record of paying dividends.

However, it is starting to show signs of being a major beneficiary of China's growing demand for air travel and I expect that revenues (from all sources) will continue to rise for some time. Simply doubling the interim result suggests a 2011 PE of around 15 and a return to paying dividends on a regular basis (although at very modest levels initially). Essentially I am betting on BCIA being able to grow its revenues for a number of years. The nature of the asset and its monopolistic status give me some comfort on the gearing.

In terms of personal experience, given that delays in arrival and departure times are routine, I would expect that BCIA will need to spend some money on expanding capacity to meet rising demand at some stage. The potential for future CAPEX and the maturity profile of the existing debt are my two main concerns.

I paid HK$4.27 per share.

However, it is starting to show signs of being a major beneficiary of China's growing demand for air travel and I expect that revenues (from all sources) will continue to rise for some time. Simply doubling the interim result suggests a 2011 PE of around 15 and a return to paying dividends on a regular basis (although at very modest levels initially). Essentially I am betting on BCIA being able to grow its revenues for a number of years. The nature of the asset and its monopolistic status give me some comfort on the gearing.

In terms of personal experience, given that delays in arrival and departure times are routine, I would expect that BCIA will need to spend some money on expanding capacity to meet rising demand at some stage. The potential for future CAPEX and the maturity profile of the existing debt are my two main concerns.

I paid HK$4.27 per share.

CKI purchased

This morning I added a few more shares in CKI (HK:1038) to the portfolio. The shares offer a reasonable dividend of around 3.2% with reasonable prospects for that to grow over time. I paid HK$46.95 for the additional shares.

Tuesday, March 13, 2012

A few observation on a trip to London

I have just returned to Hong Kong after a week spent in London on business. A few random observations:

1. The flights in both directions were full with waiting lists for business class. Given how inflated business class has become, I can't see myself doing much flying in business class once I have to lay for it myself;

2. The parts of London I was in seemed to be doing well and there was a general feeling of optimism regarding economic prospects. As I was mostly confined to the better areas of central London and dealing with people from the top tax bracket who were either bankers or people who provide services to banks. The negatives were largely connected with government revenue grab and the on-going Euro zone issues;

3. There was universal pessimism about London's ability to be ready for the Olympics and considerable condemnation of the way the preparations have been managed;

4. London real estate is very expensive;

5. Even with 20% VAT many consumer goods are much cheaper in London than they are in Hong Kong - including made in China sports shoes (about 30-40% cheaper) and books;

6. I loved Foyles and Waterstones book stores - I really really hope these stores survive for the longer term (unlike many book stores in other countries which have failed I the face of digital books and on-line order facilities);

7. The much vaunted London curries were not as good as the ones I can get in Hong Kong. Tapas and pub food were much better;

8. The traffic was terrible (as usual);

9. The live theatre/entertainment/gallery etc space was fabulous.

Of course, all this is off the back of a small sample size - one vistor's business trip - but, on the whole, I was impressed and hope to spend more time there post retirement.

1. The flights in both directions were full with waiting lists for business class. Given how inflated business class has become, I can't see myself doing much flying in business class once I have to lay for it myself;

2. The parts of London I was in seemed to be doing well and there was a general feeling of optimism regarding economic prospects. As I was mostly confined to the better areas of central London and dealing with people from the top tax bracket who were either bankers or people who provide services to banks. The negatives were largely connected with government revenue grab and the on-going Euro zone issues;

3. There was universal pessimism about London's ability to be ready for the Olympics and considerable condemnation of the way the preparations have been managed;

4. London real estate is very expensive;

5. Even with 20% VAT many consumer goods are much cheaper in London than they are in Hong Kong - including made in China sports shoes (about 30-40% cheaper) and books;

6. I loved Foyles and Waterstones book stores - I really really hope these stores survive for the longer term (unlike many book stores in other countries which have failed I the face of digital books and on-line order facilities);

7. The much vaunted London curries were not as good as the ones I can get in Hong Kong. Tapas and pub food were much better;

8. The traffic was terrible (as usual);

9. The live theatre/entertainment/gallery etc space was fabulous.

Of course, all this is off the back of a small sample size - one vistor's business trip - but, on the whole, I was impressed and hope to spend more time there post retirement.

Wednesday, March 07, 2012

A very short vacancy

As mentioned in the monthly review, one of our properties became vacant at the end of February. I have already found a new tenant who will move in mid month meaning that I have only a two week vacancy (which is about the best that can be reasonably expected). It also means that we have only two weeks to complete the tidy up work - repaint, new fridge, replace one airconditioning unit, fix some wiring, new blinds, polish floor, replace one door and a few other things. It's quite a long list and will chew up a couple of months rent but the previous tenant had been in for six years so, to a large extent, this is catch up.

The new rent is about 9% higher than what the previous tenant was paying.

The new rent is about 9% higher than what the previous tenant was paying.

Thursday, March 01, 2012

Monthly Review - February 2012

February saw the value of the portfolio continue to move higher, largely in line with the movements in equity markets and favourable exchange rate movements. Positive cash from on the properties (fully leased) and a reasonable savings rate added to the gains.

Here are the details:

1. my Hong Kong equity portfolio appreciated. I purchased shares in HKR International, Tibet 5100, NWS and CKI Holdings. I sold small positions in CMOC, AUPU and Allan International;

2. my AU/NZ equities appreciated;

3.my ETFs appreciated in line with the local markets, with all being positive. I purchased a few units in the Vitenam ETF;

4. my commodities advanced, led by silver. I made a small additional investment in silver;

5. all of my properties were occupied with all tenants paying on time. One property became vacant at the end of February. The unit has not had any substantive decoration for six or seven years so I am looking at a substantial expense and a 2-3 month vacancy;

6. currency movements were positive, as the NZD and AUD appreciated against the HKD/USD;

7. my position in bonds remains small. No bonds were purchased this month. I would like to add some more bonds to the portfolio but am finding direct purchases of bonds through the banks I have accounts with to be something of an exercise in frustration in Hong Kong;

8. I had no open derivative positions;

9. savings were moderate with very low expenses.

My cash position declined slightly due to new investments and a transfer to mrs traineeinvestor. I currently hold 55.2 months of expenses in HKD cash or equivalents. This is close to an all time high - in fact it is too high given current inflation levels and the near zero nominal yields on bank deposits.

For the month, my net worth increased by a huge 6.09%. The year to date increase is 15.68%. The year is off to a good start.

Here are the details:

1. my Hong Kong equity portfolio appreciated. I purchased shares in HKR International, Tibet 5100, NWS and CKI Holdings. I sold small positions in CMOC, AUPU and Allan International;

2. my AU/NZ equities appreciated;

3.my ETFs appreciated in line with the local markets, with all being positive. I purchased a few units in the Vitenam ETF;

4. my commodities advanced, led by silver. I made a small additional investment in silver;

5. all of my properties were occupied with all tenants paying on time. One property became vacant at the end of February. The unit has not had any substantive decoration for six or seven years so I am looking at a substantial expense and a 2-3 month vacancy;

6. currency movements were positive, as the NZD and AUD appreciated against the HKD/USD;

7. my position in bonds remains small. No bonds were purchased this month. I would like to add some more bonds to the portfolio but am finding direct purchases of bonds through the banks I have accounts with to be something of an exercise in frustration in Hong Kong;

8. I had no open derivative positions;

9. savings were moderate with very low expenses.

My cash position declined slightly due to new investments and a transfer to mrs traineeinvestor. I currently hold 55.2 months of expenses in HKD cash or equivalents. This is close to an all time high - in fact it is too high given current inflation levels and the near zero nominal yields on bank deposits.

For the month, my net worth increased by a huge 6.09%. The year to date increase is 15.68%. The year is off to a good start.

Subscribe to:

Posts (Atom)