My non-expert attempt to satisfy myself that there is in fact a bubble is set out below. The conclusion I reached is that while Hong Kong real estate is expensive my many (but not all) measures, I was struggling to find evidence that there was in fact a bubble in the Hong Kong housing market.

Characteristics of a bubble

Looking at the definition of "bubble" it is fairly obvious that at least some of the key characteristics of a bubble are absent. In particular transaction volumes are subdued (and have been since the government's cooling measures) rather than "high". Also, while expensive (see below) prices have at least a reasonable connection with intrinsic values - with short term speculators (flippers/confirmors) being largely excluded from the market, most buyers are either end users or longer terms investors. That buyer profile is not consistent with the crowd of frothy speculators

It's also worth mentioning that the high levels of gearing commonly associated with real estate bubbles is notably absent. HKMA and bank imposed deposit requirements are high and many buyers are paying cash. Higher interest rates would be unlikely to result in a large number of distressed mortgagors.

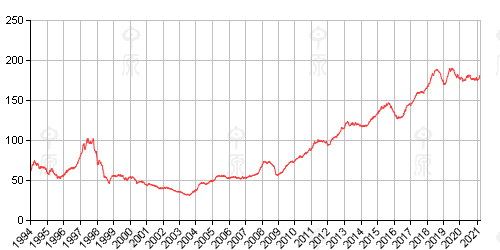

Property price index

The leading index for the residential secondary market is the Centa-City Leading Index (CCL) published by Centadata which is available here. The chart below shows the CCL from 1994 through to 23 March, 2012.

It's worth noting that the CCL is based on actual sales prices in the secondary market. In other words it is a nominal index rather than a real (inflation adjusted index). Using Hong Kong CPI as a measure of inflation:

The CPI data is from Trading Economics which has some neat interactive features.

Very roughly, if the index was rebased to 1994 dollars, it would lower the 2012 value of the CCL by about 25.8% or from 99.17 to 78.83 and 1997's base CCL of 100 by 22.7% to 81.5%. In other words, from 1994 to 2102 in real terms the CCL rose from 63 to 99.17 (57.4%) in nominal terms and from 63 to 78.83 (25.1%) in inflation adjusted terms. Quite frankly, that's not much of a gain over a period of 18 years, especially when the expansion of Hong Kong's economy is taken into account. The compound annual increase in the value of the CCL (in either nominal or real terms) is small.

While it is just about always possible to quibble with the methodology used to construct an index, for present purposes, the only thing I will mention is that the CCL does not adjust for the size effect (the fact that larger properties typically sell for more per square foot than smaller ones). While I could not find any data tracking the average size of apartments in Hong Kong, anecdotally I understand that the average size has increased over time, although not by much. An adjustment to account for the size effect would reduce the rate of increase in the CCL.

Put differently, I would need to cherry pick the low point in the CCL in 2003 to show a reasonably high rate of annual increase in the CCL (and given that 2003 coincided with the end of the Asian Financial Crisis and SARS, it would indeed be an exercise in cherry picking the data).

Affordability

One way to measure whether real estate is expensive is affordability. Leaving aside reports like the one included in this article which are based on seriously flawed comparisons (at the very least there would need to be adjustments for differential tax rates and differential living costs - and in both respects Hong Kong does very well with most income earners paying no tax and not being burdened by the high cost of owning and running one or more private cars), it would appear that housing affordability today is much better than it was in 1997 (a combination of much lower interest rates and higher incomes) but worse than it was at the low point in 2003.

Given that (IMHO) high deposit requirements distort affordability comparisons even within Hong Kong, there isn't much point in debating the exact measures of affordability beyond the generalisations above. That said, it is not possible to claim that there is a bubble based on measures of affordability.

Other indicators

There is no denying that Hong Kong real estate is expensive in both absolute and relative terms. Hong Kong residential prices usually rank in the upper echelons of the global price bracket alongside cities like London and New York. Given Hong Kong's small size and status as a substantial financial centre, this is hardly surprising. Being expensive on a global comparative basis but no more so than several other cities does not a bubble make.

Yield is one yard stick used by investors to evaluate property as an investment. At the moment, gross yields on unfurnished mid-market units in good areas like Mid-Levels are in 3-5% range. Net yields are obviously lower and there is considerable variation between properties (as you would expect). Yields this low in an environment where inflation is 4.7%, bank deposit rates are negligible and mortgage rates are around 2.25% are both understandable and unexciting. In other words, it is possible to use at least some gearing and be cash flow positive on an investment property.

Conclusions

After going through the exercise, I failed to find anything that justified characterising Hong Kong's property market as a 'bubble' - none of the usual features of a bubble are present.

That said, real estate here is expensive (especially in the luxury sector) and I don't see enough value in the local market to justify adding to the portfolio. Given the political climate and the government stance on the property market as well as macro factors it is easy to see prices falling to some extent - how much is anybody's guess (and plenty of people are guessing). Given that affordability remains high and interest rates very low, it's also not beyond the realms of possibility that prices could go higher as well. Quite frankly, I have no idea.

Implications

As far as the implications of this exercise for my own investments are concerned, there aren't any. We will continue to hold our properties, collect the rent and reluctantly make the mortgage payments. We are unlikely to buy again at these levels - the value just isn't there. If prices drop far enough, we'd consider buying again. (And it goes without saying that just because prices drop by a meaningful amount in the future, that does not in any way validate claims that we have a bubble today.)

4 comments:

The recent Demographia survey compares affordability with annual family TAKE HOME income (they refer to it as disposable income)

A HK family would need 12+ years of their entire disposable income to pay for a house

The next highest was Australia where in the 3 biggest cities a family would need just under 6 years.

You call yourself an analyst?

You are putting out crap.

Thank you for your comment.

I am aware of the demographic surveys.

There's a summary here: http://www.cdeclips.com/en/hongkong/fullstory.html?id=59331

I'm also aware that they are heavily flawed in a number of respects which substantially devalue their validity both in comparative and absolute terms. Examples include the fact that they are based on gross household income which ignores taxes and makes low tax jursidictions look comparatively more expensive, they ignore the impact of other spending patterns (e.g. people in Hong Kong spend far less on transport than they do in places like Australia and the difference is material) and the effect of housing assistance which has a huge impact on affordability and varies hugely from country to country. There are other points as well. I still conclude that property here is very expensive, but the extent of the "unaffordibility" is overstated to an uncertain degree.

There's a debate going on at the moment on AsiaEXPAT on this topic - feel free to join the discussion.

I'll stick with my view that HK property is expensive, does not represnt good value but is not a bubble.

Lastly, I'm not an analyst (please see the disclaimer on the front page). In fact I have no qualifications as an investor. I'm just a guy hoping to make enough money to take a comfortable early retirement - so far so good.

I really do appreciate people challenging my efforts and/or pointing out where I may have gone wrong - it helps me learn.

If you do comment again, please feel free to be as critical as you like....but without the swearing.

Cheers

Traineeinvestor

Traineeinvestor,

Thank you for the thoughtful assessment of the Hong Kong property market. I also commend your reply to the previous post. I am sick of reading comments that descend into verbal assults and thought you dealt with abusive comment positivley. Keep writing!

@ Anonymouns#2

Thanks for dropping by and for your encouragement.

Comments are always welcome - especially ones which challenge my views. My take on the market is no better (and possibly worse) than anyone else's.

Cheers

traineeinvestor

Post a Comment